據(jù)IFR預計,2021年我國工業(yè)機器人市場規(guī)模將達到445.7億元;到2023年,國內(nèi)市場規(guī)模進一步擴大,預計將突破589億元。

隨著國際上各領(lǐng)域正逐步向智能化方向發(fā)展,AI技術(shù)正深入到不同的行業(yè)中,在工業(yè)制造上,機器人的參與開始成為主流,但遺憾的是,長期以來工業(yè)機器人都被國際上四大家族所掌控,他們都是何方神圣呢?

在日本和歐洲地區(qū),由于勞動力不足,所以催生了很多的智能化產(chǎn)品來實現(xiàn)人工替代,這期間逐漸孕育出了4個實力雄厚的機器人生產(chǎn)商。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

nce="true" class="jsx-2558377382 pictureBottomBtn" style="box-sizing: inherit; color: rgb(83, 123, 255); background: rgb(240, 246, 255); line-height: 34px; text-align: center; font-size: 14px; margin: 0px auto; overflow: hidden; text-overflow: ellipsis; border-bottom-left-radius: 4px; border-bottom-right-radius: 4px; border-top: 4px solid rgb(240, 246, 255); z-index: -1; transform: translateY(-4px); max-width: 619px;">打開騰訊新聞,查看更多圖片 >

從2011年開始,來自日本的安川電機以及發(fā)那科,還有德國的庫卡和瑞士的abb,這四家企業(yè)聯(lián)手開創(chuàng)了工業(yè)機器人的新時代,并拿下了全球80%的市場份額。

他們的技術(shù)無一例外都能夠?qū)崿F(xiàn)高精尖產(chǎn)品的生產(chǎn),而且產(chǎn)業(yè)鏈和供應(yīng)體系非常完備,經(jīng)常會互通有無,儼然打造出了該領(lǐng)域難以逾越的技術(shù)屏障。當時國內(nèi)也看中了工業(yè)機器人的發(fā)展前景,無奈不管是技術(shù)還是設(shè)備都被這四大家族所壟斷

只能在一些簡單工業(yè)品領(lǐng)域研發(fā)一些低端機器設(shè)備。

只能在一些簡單工業(yè)品領(lǐng)域研發(fā)一些低端機器設(shè)備。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

全球工業(yè)機器人已基本形成以日、美、韓、德、中為主導的發(fā)展格局,“四大家族”市場占有率超過50%。工業(yè)機器人存量穩(wěn)定增長,國內(nèi)工業(yè)機器人裝機量居世界首位,但裝機密度仍然較低。市場對搬運和焊接功能需求最大,重點應(yīng)用領(lǐng)域是汽車與電子設(shè)備制造。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

我國工業(yè)機器人產(chǎn)業(yè)經(jīng)歷4個階段,從研究與樣機開發(fā)逐漸形成產(chǎn)業(yè)集群,核心零部件國產(chǎn)化正在加速。據(jù)IFR預計,2021年我國工業(yè)機器人市場規(guī)模將達到445.7億元;到2023年,國內(nèi)市場規(guī)模進一步擴大,預計將突破589億元。國內(nèi)機器人產(chǎn)業(yè)主要集中于華東、華南地區(qū),通過產(chǎn)業(yè)園區(qū)形成產(chǎn)業(yè)聚集。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

目前,國內(nèi)市場仍以日本品牌為主的外資廠商主導,但外資品牌占比逐年降低;國產(chǎn)自主品牌的競爭力同質(zhì)化問題改善,逐漸分化成三大梯隊,其中埃斯頓、新時達、埃夫特等廠商技術(shù)和市場競爭力較強,位列第一梯隊。

根據(jù)機械結(jié)構(gòu)的特點,可以將工業(yè)機器人劃分為4類,垂直多關(guān)節(jié)和協(xié)作機器人的工作范圍最廣,其中裝配是較為普遍的應(yīng)用場景。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

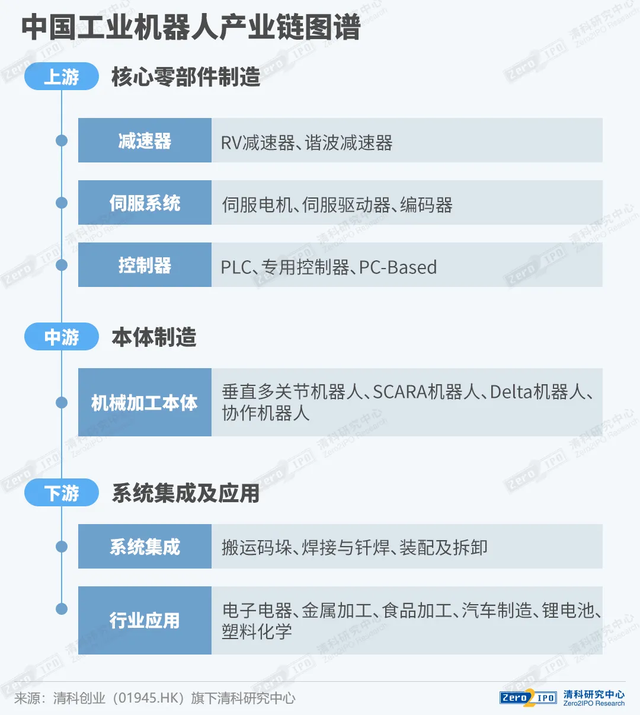

從產(chǎn)業(yè)鏈各環(huán)節(jié)看,1)上游:減速器,技術(shù)壁壘在工業(yè)機器人核心零部件中最高,RV減速器國產(chǎn)化難度較高,納博特斯克在全球市場占有率領(lǐng)先,諧波減速器國產(chǎn)化率較高,國內(nèi)以綠的諧波為首的多家廠商已實現(xiàn)量產(chǎn);伺服系統(tǒng),國內(nèi)市場份額長期被外資品牌占據(jù)主導地位,

國產(chǎn)品牌的市占率穩(wěn)步提升;控制器,國內(nèi)市場份額主要由外資企業(yè)占據(jù),技術(shù)難度較低,控制器市場主要的增量來自于國產(chǎn)廠商,聚焦于中低端應(yīng)用領(lǐng)域。2)中游:本體制造,包括支柱、底座、手臂、腕部等,以多關(guān)節(jié)機器人和scara機器人為主。3)

下游:系統(tǒng)集成-搬運和焊接等應(yīng)用占比較高;應(yīng)用行業(yè)-汽車制造和電子電氣占比較高;應(yīng)用場景從汽車等領(lǐng)域逐步轉(zhuǎn)向通用制造及新興產(chǎn)業(yè),國內(nèi)增量市場空間廣闊。

國產(chǎn)品牌的市占率穩(wěn)步提升;控制器,國內(nèi)市場份額主要由外資企業(yè)占據(jù),技術(shù)難度較低,控制器市場主要的增量來自于國產(chǎn)廠商,聚焦于中低端應(yīng)用領(lǐng)域。2)中游:本體制造,包括支柱、底座、手臂、腕部等,以多關(guān)節(jié)機器人和scara機器人為主。3)

下游:系統(tǒng)集成-搬運和焊接等應(yīng)用占比較高;應(yīng)用行業(yè)-汽車制造和電子電氣占比較高;應(yīng)用場景從汽車等領(lǐng)域逐步轉(zhuǎn)向通用制造及新興產(chǎn)業(yè),國內(nèi)增量市場空間廣闊。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

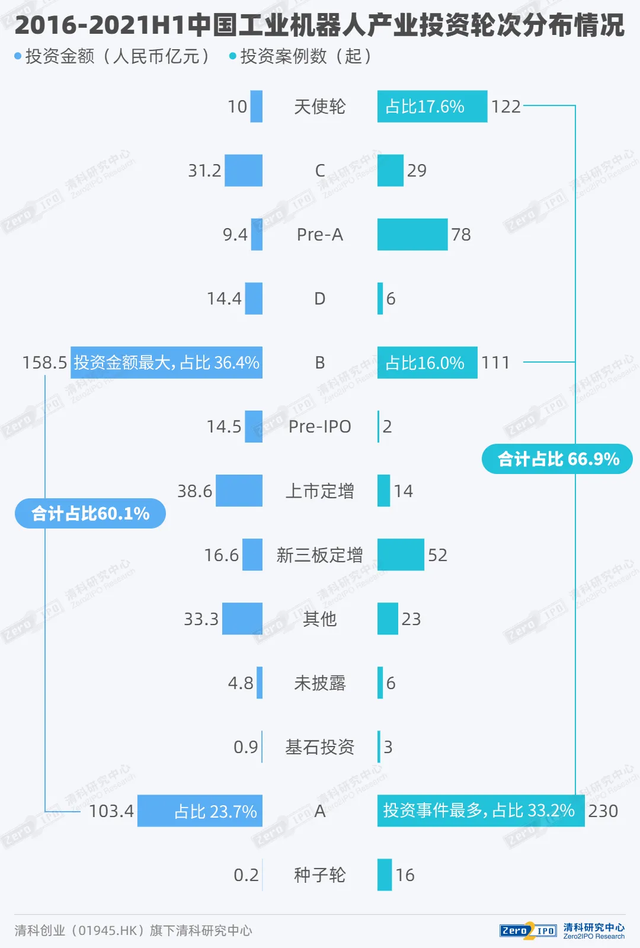

根據(jù)清科創(chuàng)業(yè)旗下PEDATA MAX數(shù)據(jù),2016-2021H1,中國工業(yè)機器人領(lǐng)域披露投資事件692起,披露投資金額約435.9億元;零部件制造和集成應(yīng)用環(huán)節(jié)投資熱度較高;A輪、天使輪及B輪案例數(shù)合計占比近7成;廣東、北京和長三角地區(qū)是熱點地域。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

整體來看,工業(yè)機器人下游多應(yīng)用領(lǐng)域滲透率逐年提升,“機器人換人”成必然趨勢;工業(yè)機器人在核心零部件、共融技術(shù)、云化技術(shù)等方面不斷進步優(yōu)化;進口替代進程加速,國產(chǎn)廠商份額持續(xù)上升;工業(yè)機器人領(lǐng)域披露投資金額逐年增長,投資熱度保持上升趨勢。

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">

nce="true" class="jsx-2558377382 image-wrap" style="box-sizing: inherit; position: absolute; inset: 0px; background-color: rgb(234, 234, 234); background-image: url("//mat1.gtimg.com/qqcdn/xw/20211215/images/image-placeholder-logo.png"); background-size: 45px 45px; background-position: center center; background-repeat: no-repeat; border-radius: 4px;">